Blog

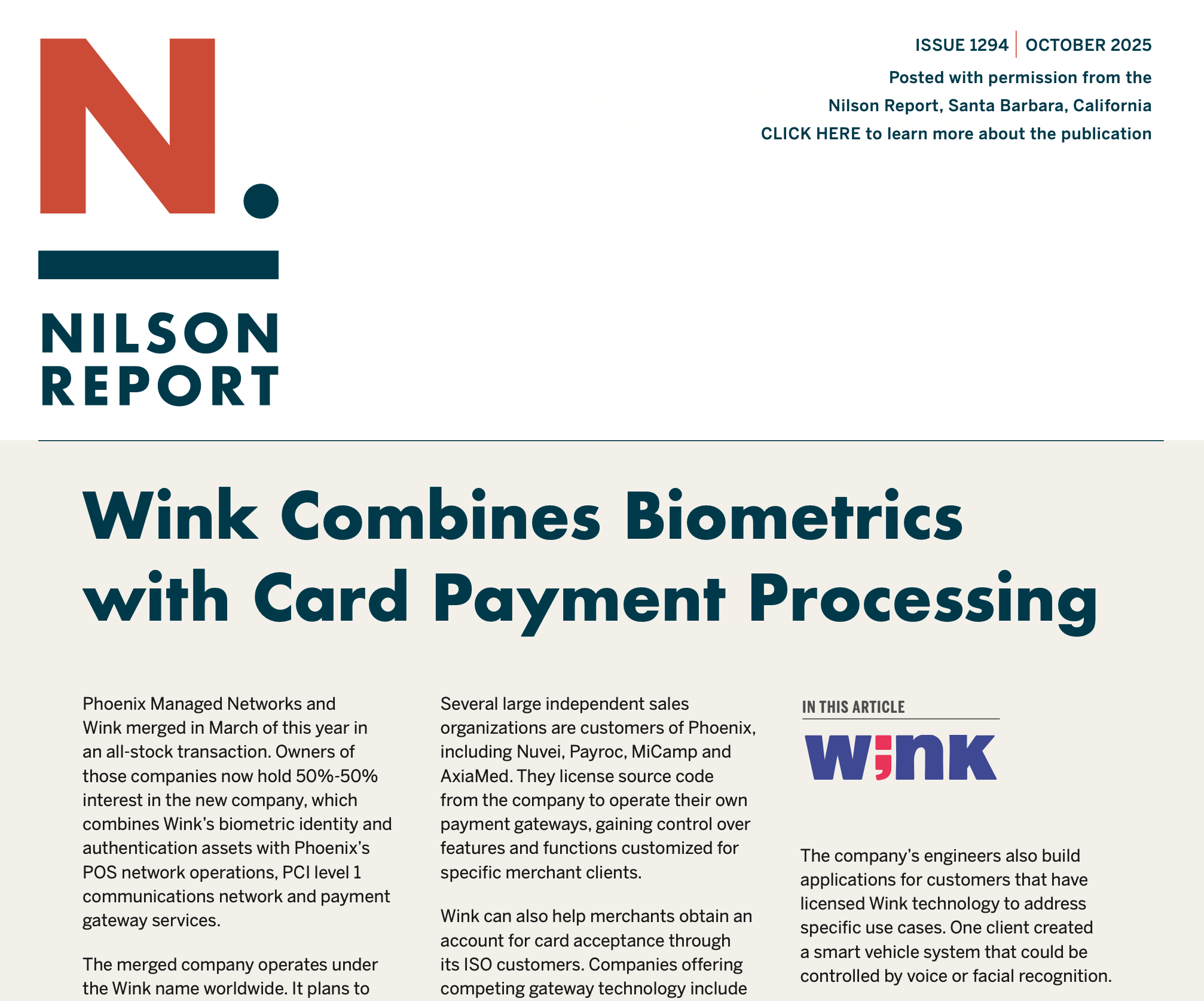

Wink Featured in The Nilson Report | Biometrics with Card Payment Processing

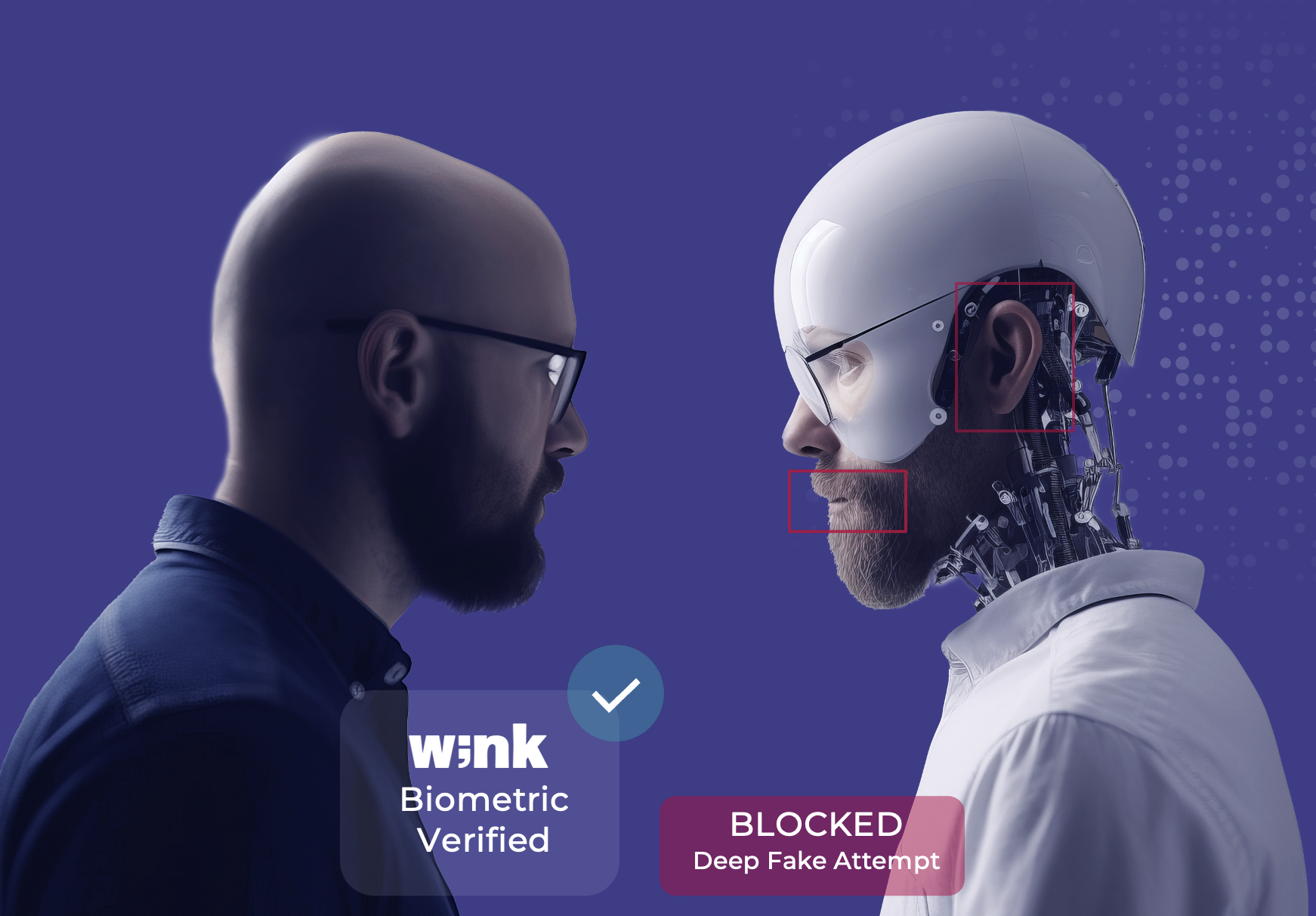

For decades, payments have revolved around the card number. Swipe, dip, tap - the form factors changed, but the underlying credential stayed the same. That’s shifting. Biometric authentication is no longer a novelty at the airport or on your phone; it’s rapidly becoming the default for how we pay, both online and in-person. And the real leap forward isn’t just replacing a password with a face - it’s moving toward invisible, continuous, multimodal authentication that makes checkout seamless and fraud far harder.

The numbers speak for themselves. Juniper Research estimates that biometric payments on mobile devices alone will reach $3 trillion annually by 2025, up from less than $250 billion in 2019.¹ Face and fingerprint are leading the charge, but new modalities - palm vein, voice, behavioral biometrics - are expanding the options. Adoption is accelerating because it delivers a simple equation that merchants and banks understand: fewer false declines, faster lines, lower fraud.

What’s coming next is “invisible payments.” The consumer doesn’t reach for a card or type a CVV; identity is the credential, verified passively in the background. Amazon One is an early proof point, with palm-based payments rolling out across stadiums and retail. Combine that with the push toward passkeys - device-bound credentials tied to a face - and you have a checkout flow that eliminates manual entry altogether. This isn’t science fiction; it’s already live in pilot deployments, and consumers are showing willingness to adopt. Roughly 38% of people already use facial recognition to access banking apps, with another 32% saying they would if offered.²

The real unlock is multimodal. By combining factors - face plus palm, or voice - pushes the security profile to near-zero fraud. At the same time, continuous authentication models are emerging: systems that re-verify identity throughout the session, not just at login. For payments, this means keeping fraudsters out not just at the point of sale, but during account takeover or mid-transaction attacks.

Of course, the challenges are real. Privacy regulations are uneven across markets. And consumers need education on how their biometric data is stored, protected, and never re-used for purposes they didn’t authorize. But the trajectory is clear: the payment ecosystem is moving beyond fragile card numbers toward trusted identity. The winners will be the banks and merchants who make that shift seamless, secure, and invisible to the end user.

At Wink, we see this as the natural next chapter. Payments anchored in biometric identity won’t just be faster or safer; they’ll be the connective tissue for loyalty, fraud prevention, and customer experience. The transition is happening now, and those who embrace invisible payments today will be positioned to lead in a market where identity is the new currency.

¹ Juniper Research, 2023 forecast on biometric mobile payments

² iProov Biometric Adoption Study, 2024

We’re honored to be recognized by The Nilson Report for our work at the intersection of biometrics, payments, and AI-driven commerce.

Read more about The Nilson Report here (subscription required).

Explore Wink’s biometric and payment solutions at www.wink.cloud.